The UK has become the world’s fourth largest exporter, but can it...

UK business is beaming with pride with the recent news of the country’s emergence as the fourth largest exporter in...

READ MORE UK UK

UK UK

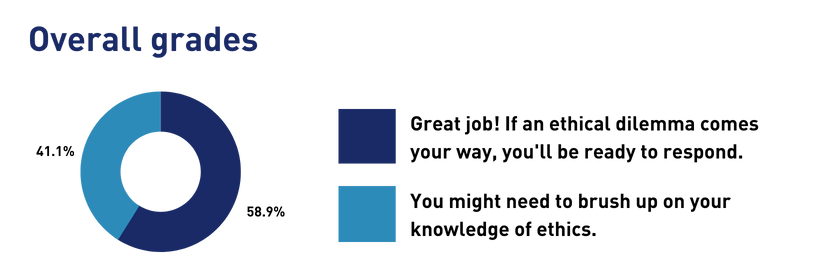

Our most recent quiz found that six in 10 respondents were ready for an ethical dilemma. Here are the full results and where to brush up.

The recent ethics quiz was our toughest yet – asking how readers would respond in a series of scenarios, and testing knowledge about the fundamental principles of ethical frameworks and where to turn for help.

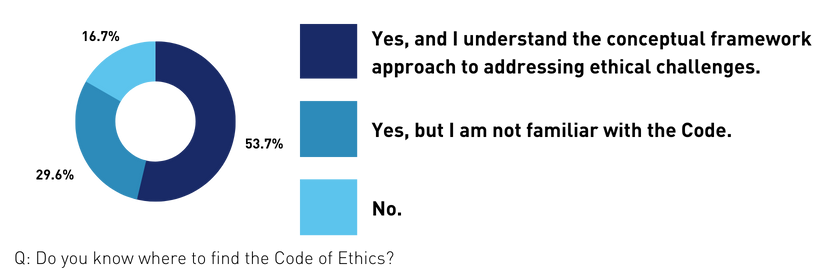

Just over 16% of respondents didn’t know where to find the Code of Ethics, and a further 29.6% were not familiar with it.

At the beginning of this year, the IFA adopted the Code of Ethics for Professional Accountants of the International Ethics Standards Board for Accountants (IESBA) published by the International Federation of Accountants (IFAC). This Code of Ethics provides an ethical framework for accountants to operate within.

IFA bye-laws require members, students, affiliates and firms to comply with the Code of Ethics – familiarity with it is a start.

The IFA Code of Ethics is available on the IFA website.

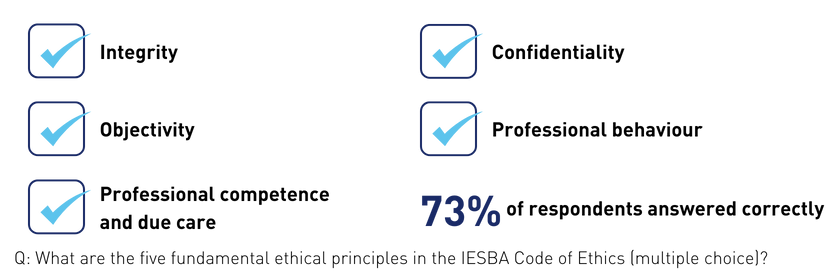

The Code sets out five fundamental principles, which should guide members’ behaviour, and 73% of respondents recognised these five principles.

These principles are useful in assessing any threats to ethical behaviour and compliance with ethics requirements, and should guide members in implementing safeguards.

The quiz also asked about the possible threats to the five fundamental principles. Just 41.1% of respondents answered all five correctly. The most common mistake respondents made was including ‘self review’ as a threat – and while it is not officially on the list, it isn’t a bad ‘orange flag’ to keep in mind.

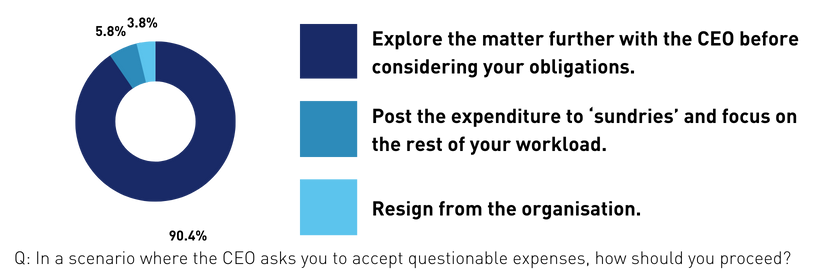

Respondents were clear on this one – when presented with a scenario of a CEO asking an accountant to post questionable expenses to ‘sundries’, 90.4% said they would ask the CEO more questions and consider their obligations.

Almost 6% would do as instructed and move on, and almost 4% would resign.

And while resigning seems like it’s a get-out-free card, the ethical framework does not support this course of action. The only acceptable action in this case is to explore the matter further and consider ethical obligations.

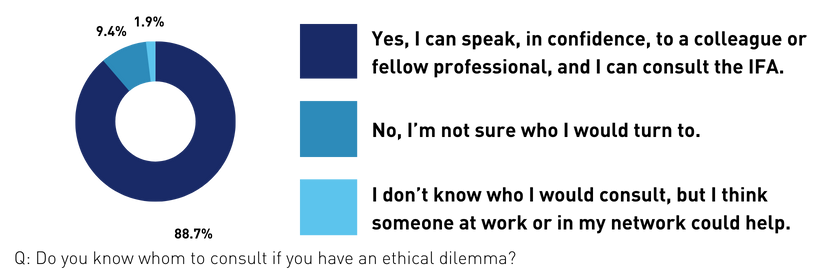

Just under 10% of respondents would not immediately know who to turn to with an ethical quandary.

While those in larger practices might find it simple to knock on a colleague’s door, we know this is a particular challenge of sole operators. We recently spoke with Professor Chris Cowton at the Institute of Business Ethics about this.

“You have got to invest in training or make sure you serve your client by bringing in the right people at the right time, whether it is sending the client somewhere else or collaborating with another practice,” suggests Cowton.

The IFA team is also on hand to support members in need of ethics advice – contact us here.

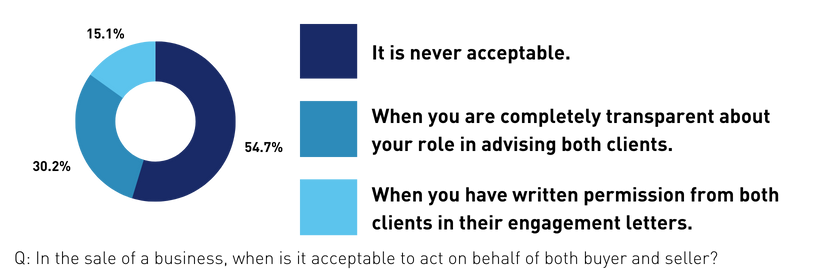

Finally, the quiz revealed an important point to clarify – just under half of respondents told us that there are circumstances in which it is acceptable to represent both the buyer and seller in the sale of a business.

It is not.

UK business is beaming with pride with the recent news of the country’s emergence as the fourth largest exporter in...

READ MORE

In 2022, Emirati national Abdulla Alfalasi was jailed for nine years, following a conviction for leading the biggest...

READ MORE

We spoke with IFA Director of Professional Standards Tim Pinkney about how firms can best prepare for compliance...

READ MORE