HMRC umbrella company ‘checking tool’ looms for workers

Umbrella company consultation response and guidance due from HMRC, as more details come out on Tax Administration and...

READ MORE UK UK

UK UK

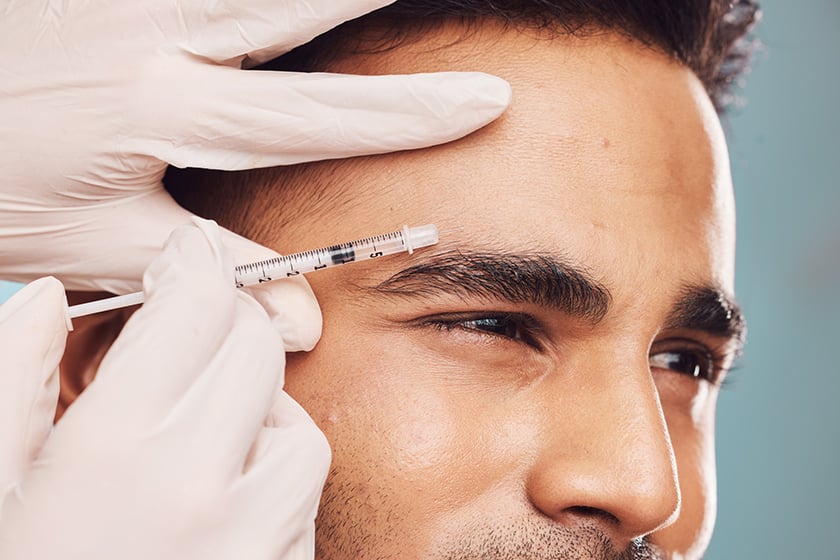

The recent outbreak of cosmetic clinics offering everything from nail fungus treatment to chemical peels has created grey areas around VAT exemption. Closer inspection by HMRC has confirmed that for these clinics, the prognosis could be negative.

Several skincare and other clinics have made headlines recently – at least within publications involved in accounting and tax matters – for their attempted and failed stances on VAT exemption.

Skin Rich Ltd, for example, argued that Botox, dermal filler treatments and fungal nail treatments should be considered VAT exempt, as they’re medical procedures, “principally to protect, restore or maintain the health of an individual”, as tax advisers Marcus Ward Consultancy explained in its summary of the case.

The case heard in the First-Tier Tribunal resulted in a ruling that said the treatments were not medical procedures and did not meet the requirements for VAT exemption.

Another business, Illuminate Skin Clinics, offered “aesthetic treatments such as Botox, skincare, chemical peels and platelet-rich plasma treatments”, accountingWEB reported.

The company’s sole director was its founder Dr Sophie Shotter, an anaesthetist and member of the General Medical Council. Certain sales had been treated as VAT exempt, “on the basis they qualified as medical care”.

In this instance, the First-Tier Tribunal case found customers had generally not been referred by another health professional. They often came to the clinic with a request for a particular treatment typically unrelated to other medical conditions. A person with depression, for example, came to the business for a skin-tightening procedure.

Therefore, in several cases it was decided the exemption conditions were not met.

This second case was particularly interesting as services were provided within the scope of Dr Shotter’s medical registration. The issue was that the process typically did not involve referral, diagnosis of a medical issue or the development of a treatment plan.

Over the past five to 10 years, says Ian Hornsey, Managing Director of Devonports LAS Accountants & Business Advisors, Chair of the IFA Member Advisory Committee and IFA Regional Ambassador for Eastern England, there has been an explosion of high street treatment clinics in the UK.

“Even here, in Southend-on-Sea, I’d say 20 to 30 clinics have opened in the past two years alone,” he says. “If you multiply that across the country, suddenly there are all of these clinics.”

Ian points out that many have developed out of beauty salons and hairdressers.

“Suddenly we have a situation where owners of some of these clinics believe that because a procedure has to do with your skin, it can be considered a medical procedure. But actually, we’re seeing a situation where people go to the clinic because they want something removed from their skin, or they want their skin tightened.”

And that point – the customer going into the interaction having made a specific choice already and seeking a specific outcome – makes a difference to VAT exemption eligibility.

“That’s where the tribunal has made the decision that they’re not exempt from VAT,” Ian says.

Typically, if a customer makes a choice to go to such a clinic and doesn’t require referral via their GP or another medical specialist, the procedure is immediately unlikely to meet the criteria for VAT exemption.

If the process is not administered by a registered medical professional working within their field (a dentist can’t be doing work on or around people’s eyes, for example), that’s another strike against VAT exemption eligibility.

Finally, if detailed records are not kept, records that prove the procedure was directly related to a treatment plan for a properly diagnosed medical issue, that’s a third strike.

“A VAT Tribunal case involving HMRC and a skin clinic in June 2023 confirmed that a variety of aesthetic, cosmetic, skincare and wellness treatments did not qualify as VAT-exempt health or medical treatment,” Ian says.

The decision in that case does not rule out VAT exemptions in all cases of skin-related treatments, but it does confirm that any medical treatment does need to meet stringent criteria to qualify for exemptions.

“The professional should diagnose, assess and document the patient’s needs, and be able to demonstrate if necessary the primary health purpose,” Ian says.

“Medical professionals providing skin, cosmetic, aesthetic and similar treatments should discuss with an accountant or VAT adviser their full specific circumstances to determine the VAT position of their procedures.”

Umbrella company consultation response and guidance due from HMRC, as more details come out on Tax Administration and...

READ MORE

National insurance, income tax, VAT, capital gains tax, inheritance tax… it’s easy to get confused about the many...

READ MORE

Cryptocurrencies are surging again. Bitcoin has just hit an all-time high of more than US$72,000 (£56,300), pushing...

READ MORE